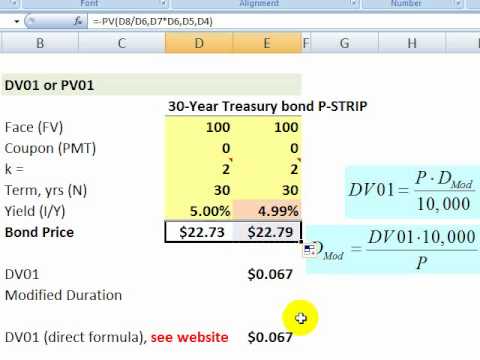

The DV01 gives us the dollar change in bond price for a one basis point decline in the rate. We typically assume yield (YTM) is the rate change, so as Tuckman …

Images related to the topic d v financial

Bond DV01 and duration

Search related to the topic Bond DV01 and duration

#Bond #DV01 #duration

Bond DV01 and duration

d v financial

See all the latest ways to make money online: See more here

See all the latest ways to make money online: See more here